Steel Abrasives Monthly Market Update: February 2026

Focus: Price Drivers & Key Regional Markets

Date of issue: 28 February 2026

Period covered: February 2026

1. Scope & Methodology

This report provides an objective summary of February 2026 market conditions relevant to steel abrasives (cast steel shot, cast steel grit, stainless steel shot and conditioned cut wire).

Because there is no dedicated global price index for steel abrasives, price assessments in this report are based on:

- Movements in scrap steel (especially CFR Turkey benchmarks) and flat steel (HRC); (Lme)

- Trends in ocean freight rates on key trade lanes, using the Drewry World Container Index (WCI); (Drewry)

- Exchange rate developments for RMB vs USD; (经济交易所)

- Global and regional steel demand and production indicators from the World Steel Association and other industry sources; (worldsteel.org)

- Publicly available information on China’s steel scrap market (e.g. Mysteel summaries). (MySteel)

Steel abrasives pricing typically follows steel scrap and HRC trends with a lag, adjusted for energy, labour, packaging and logistics. All conclusions below are descriptive and do not constitute any commercial offer or quotation.

2. Global Price Trends & Cost Drivers

2.1 Benchmark Price Movement

In February 2026, key steel-related benchmarks showed a pattern of continued firmness, extending the uptrend seen in late 2025:

- Global ferrous scrap: The LME Steel Scrap CFR Turkey (Platts) February contract was around USD 376–377/t as of 26–27 February, compared with levels closer to USD 370/t in late 2025, implying roughly a 2–3% month-on-month increase and a clear continuation of the Q4–Q1 recovery. (Lme)

- Hot-rolled coil (HRC): The global HRC benchmark rose to about USD 1,011/t on 27 February 2026, up around 4% over the past month and roughly 11% higher year-on-year. (经济交易所)

- In the US, Midwest HRC futures through mid-February traded mostly in the USD 975–1,000/t range, reinforcing the picture of a firm but not explosive flat-steel market. (Investing.com)

Taken together, underlying steel input costs in February moved moderately higher again. For steel abrasives producers, this adds incremental upward cost pressure compared with Q4 2025, though market feedback still suggests selective price adjustments, not broad, aggressive increases.

2.2 Raw Material Costs (China Focus)

From the perspective of a China-based producer, the two most important variable cost drivers in February 2026 remained:

- Domestic steel scrap prices, and

- Industrial electricity tariffs.

2.2.1 Domestic steel scrap prices

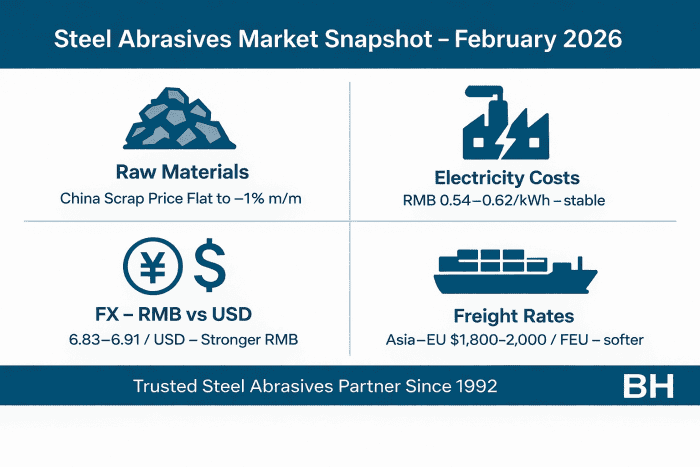

Mysteel’s February reports indicate that China’s steel scrap market has been broadly stable to slightly softer, with no abrupt moves:

- Regular Mysteel updates for “steel scrap prices: China’s major cities” and “scrap procurement prices: major mills” in late February show prices still quoted in a narrow band and described as weak but orderly. (MySteel)

- Compared with late 2025, there is no sign of a sharp rebound or collapse. Mills continue to manage scrap purchases carefully in line with reduced crude steel output and cautious finished-steel orders.

Although detailed price levels require subscription access, the available commentary supports the following qualitative view for February:

- Average domestic scrap prices are roughly flat to slightly down vs January, after the more pronounced softening seen in Q4 2025.

- The market is still influenced by lower crude steel production and disciplined supply, which limit both upside and downside.

For scrap-based steel abrasives producers in China, February’s scrap trend can therefore be summarised as “stable with a slight downward bias”, providing modest cost relief relative to the rising international benchmarks for scrap and HRC.

2.2.2 Industrial electricity tariffs

For steel abrasives production, electricity remains a significant but smaller cost component than scrap. Public data and tariff comparisons suggest that China’s industrial power prices have stayed broadly stable into early 2026:

- Country-level comparisons still place China’s business/industrial power prices around CNY 0.79/kWh (≈ USD 0.11), competitive versus many manufacturing peers. (汇率查询)

- Earlier estimates of average industrial electricity costs near USD 0.088/kWh remain a reasonable reference; there have been no major policy-driven Q1 2026 tariff spikes reported for large industrial users. (argusmedia.com)

For February specifically:

- Scrap: roughly flat to slightly softer vs January, offering minor cost relief;

- Electricity: effectively unchanged, providing a stable background cost.

Overall, raw material and power costs in China exerted mild downward to neutral pressure on the steel abrasives cost base in February, partially offset by the stronger international benchmarks used in export-market negotiations.

2.3 Energy & Environmental Policy Impact (China Focus)

Energy and environmental factors in early 2026 continue to shape the upstream steel environment, mainly via production controls and capacity discipline:

- Crude steel output & policy direction

According to the World Steel Association, global crude steel production in January 2026 fell 6.5% year-on-year to about 147.3 Mt, with Asia and Oceania down 8.6%. (worldsteel.org)

Within this, China’s crude steel output for full-year 2025 dropped to roughly 960 Mt, a 4.4% decline and its lowest level since 2018, as authorities actively manage overcapacity and carbon emissions. (Reuters)

- Environmental inspections

China has reaffirmed plans to regulate steel capacity growth through 2030, and press coverage highlights ongoing output controls and inspections as tools to enforce this policy. (Reuters)

For steel abrasives producers, the implications in February were:

- No major change in energy pricing, but

- A structural environment where upstream crude steel supply is constrained, helping to prevent HRC and other flat-steel prices from falling sharply, even when downstream demand is soft.

In short, energy and environmental policy remains neutral to mildly supportive for upstream prices, but does not add a new direct cost shock for abrasives producers.

2.4 Logistics & Exchange Rates (China Focus)

For Chinese exporters of steel abrasives, February brought some relief on freight, but a stronger RMB:

Ocean freight from Chinese ports

- The Drewry World Container Index fell for the seventh consecutive week to about USD 1,899 per 40ft container on 26 February 2026, down around 1% week-on-week and well below the levels seen during the freight rebound in late 2025. (Drewry)

- Rates on Transpacific and Asia–Europe routes both contributed to this decline as carriers adjusted capacity in response to weaker cargo volumes. (Drewry)

For typical FOB Qingdao shipments, this means that February freight quotes were lower than in December–January, narrowing the FOB–CFR gap and easing landed costs for importers.

RMB exchange rate vs USD

- Trading Economics and market data indicate that USD/CNY stood around 6.86–6.87 on 27 February 2026, with the yuan strengthening by about 1–1.3% over the past month and nearly 6% over 12 months. (经济交易所)

- Daily data show intramonth fluctuations between roughly 6.91 and 6.83, with late-February levels near the stronger end of that range. (Wise)

For Chinese exporters:

- Freight: February’s lower container rates reduced logistics cost pressure compared with late 2025.

- FX: A stronger RMB continues to compress RMB-denominated margins on USD-priced exports unless prices are adjusted.

Net effect: logistics are slightly more favourable, while FX remains a mild headwind. Overall, logistics and FX together had a roughly neutral impact on export margins in February.

2.5 Demand-Side Factors by Segment

The demand backdrop for steel—and therefore for steel abrasives—remains one of stabilisation with regional divergence:

- The worldsteel Short Range Outlook (October 2025) still projects flat global steel demand in 2025 (~1,749 Mt) and a 1.3% rebound in 2026 to ~1.77 billion tonnes. (worldsteel.org)

- Early-2026 production data show global crude steel output down 6.5% YoY in January, confirming that mills are adjusting supply to weaker demand. (worldsteel.org)

Segment-wise implications for abrasives:

- Shipbuilding & steel structures – Infrastructure and energy projects continue to support steady plate and profile blasting volumes in many markets, although some regions (e.g. parts of Europe) are affected by trade frictions and weaker exports. (eurofer.eu)

- Foundries & castings – Demand remains mixed; export-oriented foundries in growing regions are relatively active, while others in mature markets remain cautious and work off inventories.

- Automotive & machinery – Still facing cost pressure and uncertain end-user demand, which restrains restocking of abrasives and favours just-in-time purchasing. (S&P Global)

- Stainless & aluminium finishing – Export-oriented hubs in India, Vietnam and selected ASEAN countries continue to show solid usage of stainless shot and conditioned cut wire, supported by ongoing investments and rising output. (Reuters)

Overall, February did not mark a major change in global demand. Conditions are best described as “soft but stabilising”, with growth mainly in developing Asia and MENA and continued weakness or protectionist headwinds in some developed markets.

3. Key Regional Market Overview

3.1 Europe

- Demand & trade environment:

The European steel sector continues to struggle with weak demand and trade frictions. Recent data show EU steel exports to the US fell about 30% in H2 2025 following the imposition of higher US tariffs, adding pressure on mills and downstream steel-using industries. (eurofer.eu)

- Abrasives usage:

February abrasives consumption in Europe was seasonally quiet but essentially stable.- Shipyards and structural fabricators maintained core blasting operations.

- Some foundries and machinery producers continued to operate cautiously, focusing on essential work and inventory management.

Local prices for high-carbon shot and grit were broadly unchanged vs January, with small discounts only in highly competitive tenders.

3.2 Asia-Pacific

The Asia-Pacific region remains split between a slowing China and rapidly growing developing economies:

- China

As reported by Reuters, China’s crude steel output in 2025 fell 4.4% YoY to about 960 Mt, the lowest since 2018, even as exports hit a record ~119 Mt. (Reuters)

For steel abrasives, this means no strong pull from domestic heavy industry, with many suppliers focusing increasingly on export markets.

- India & fast-growing developing markets

India is expected to remain the main growth engine, with steel demand projected to rise strongly in 2025–2026 and production forecast to increase by over 11 Mt in 2026 alone. (worldsteel.org)

This supports healthy demand for blasting media used on construction steel, pipe mills, general fabrication and automotive parts. Vietnam and some ASEAN economies are also increasing steel output and exports, which supports local abrasives consumption. (Reuters)

- Japan & Korea

Steel demand is expected to remain subdued, although certain high-value sectors (automotive, machinery) maintain stable but modest abrasives usage, with a strong emphasis on quality and process control.

Price competition in Southeast Asia continues to be intense, as buyers compare local vs imported abrasives and react quickly to FX and freight changes.

3.3 Middle East & Africa

- Demand:

Several MENA countries—notably Saudi Arabia and Egypt—remain key growth centres for steel demand, driven by infrastructure, energy and industrial projects. (worldsteel.org)

This translates into solid base demand for steel abrasives for tank, pipe and structural steel blasting.

- Market behaviour:

Buyers continue to value reliable quality, certificates and on-time delivery, but February’s lower freight rates slightly improved landed costs compared with late 2025, making imported abrasives more competitive again.

3.4 Americas

- North America

In the US, market commentary points to higher HRC prices in 2026 vs 2025, but also higher volatility, as import flows recover and new domestic capacity ramps up. (Steel Market Update)

February abrasives demand remained steady but cautious, with stockholders and end-users generally avoiding speculative inventory builds.

- Central & South America

Latin American steel demand is projected to show moderate growth from a low base, but currency volatility and political uncertainty in some countries keep purchasing patterns opportunistic and project-driven. (worldsteel.org)

4. Short-Term Outlook (March–April 2026)

Bringing the above factors together:

- Raw materials:

International scrap and HRC benchmarks are higher than in late 2025, but the pace of increase has slowed. Barring any shock, they are likely to exert moderate, not extreme, upward cost pressure into March–April. (Lme)

- China cost base:

Domestic scrap appears near a short-term floor, while electricity tariffs remain stable. This suggests a relatively steady RMB cost base for Chinese steel abrasives producers in early 2026. (MySteel)

- Logistics & FX:

Container freight rates have trended lower for several weeks, improving the cost position of exporters, while the RMB has strengthened further, slightly reducing RMB margins on USD-priced sales. The interaction of these two factors will be a key watch-point in Q2. (Drewry)

- Demand:

Global steel demand is still expected to stabilise in 2025 and grow modestly in 2026, with India and other developing economies driving most of the growth, while mature markets remain subdued and increasingly influenced by protectionist measures. (worldsteel.org)

Base case (no major shocks):

- Steel abrasives prices in most regions are likely to remain within a relatively narrow band through March–April 2026.

- Where adjustments occur, they will probably be small and selective, for example:

- Slight upward revisions on grades most exposed to international scrap and HRC strength,

- Targeted promotional pricing in markets where freight has fallen and competitive pressure is intense.

- Regional differences will mainly reflect local demand strength, freight conditions and currency movements, rather than a single global price direction.

This concludes the February 2026 steel abrasives market overview.

The report is intended solely as a neutral summary of public market information and does not constitute a price quotation, commercial offer or investment recommendation.